Bonds – A Primer (part 3) - The Government Bond Market

In our last post, “Fixed Income History and Overview”, we learned about the origin of the debt and fixed income markets. Since the prestiti in Venice started it all, governments have continued to use bonds more and more aggressively over the years in order to fund all sorts of endeavors. These bonds are typically backed by capital raised by taxing their citizens.

The size of the U.S. government bond market grows each year. It is currently estimated to be a whopping $25.7 trillion (source: TreasuryDirect.gov). That means U.S. debt is over 100% to the U.S. national GDP (source: St. Louis Fed)! There is an ever-growing supply of global bond offerings, so it is a good idea to understand their purpose, uses, and advantages both for investment and corporate cash management.

Types of Government Bonds

Government bonds come in 4 main varieties – U.S. Treasuries, Agencies, Sovereigns & Municipal Bonds. In this section we will go into detail about each of them.

U.S. Treasuries

The United States government can raise capital for operations in two ways. First, by collecting taxes and second, by issuing government bonds. The United States Treasury handles the actual issuance of bonds and the Bureau of the Fiscal Service provides oversight.

U.S. Treasuries are backed by the full faith and credit of the U.S. government. While the U.S. government could theoretically default, it’s unmatched ability to repay its debt obligations makes that scenario highly unlikely. Therefore, U.S. Treasuries are considered one of the safest assets in the world.

U.S. Treasuries have four main classifications – bills, notes, bonds and treasury inflation protected securities (TIPS).

Treasury Bills (T-bills)

Treasury bills have the shortest maturity of all U.S. Treasuries, at one year or less. The common flavors are 4, 8, 13, 26, and 52 weeks. They are what is considered a discount bond. A discount bond has no coupon associated with it. What happens is you purchase it for less than par ($100) and at maturity you receive a maturity value of $100. As long as you hold the bond till maturity you make more money than you paid.

Example:

You purchase a new issue Treasury Bill at $99.10 and when it matures it will be worth $100

Treasury Note (T-Note)

Treasury notes have longer durations than Treasury Bills, coming in tenures of 2, 3, 5, 7, and 10 years. Unlike Treasury Bills, Treasury Notes pay a coupon, which will be stated when the note is issued for purchase at auction. Owners of a Treasury note will receive interest payments two times a year (semi-annually) for the duration of ownership.

There is also a variation of a Treasury note called a floating rate note. As the name implies, the interest rate paid moves and is adjusted at set intervals. The rate and adjustment are based off of the rate of U.S. T-Bills.

It’s worth noting that the U.S. 10-year note is viewed as a strong indicator of the current and future health of the economy. If the yield of the 10-year note is falling, this indicates there could be storm clouds on the horizon. If the yield of the 10-year note is rising, this indicates economic views are trending more positively.

Treasury Bond (aka Long Bond)

Treasury bonds have the longest maturity in the U.S. market – 30 years with the coupon being paid semi-annually like a T-note.

This long maturity makes it attractive for long term investors because they can lock in a steady stream of payments and not have to worry as much about short term fluctuations. The U.S. government also likes the long maturity because it allows them to essentially refinance debt for large chunks of time when yields are low. This is the same idea as a homeowner refinancing their mortgage when rates drop.

Treasury Inflation-Protected Securities (TIPS)

TIPS have maturities of 5, 10, and 30 years. TIPS are unique because the price and payment amount changes based on inflation.

TIPS are tied to the consumer price index (CPI). When the CPI goes higher the value and payment of a TIP goes higher as well. The purpose of this type of bond is to help the owner reduce inflation risk. We discuss inflation risk later in this post.

Municipal Bonds (Munis)

Municipal bonds are issued by states, counties, cities, and other government entities. They are issued to fund day to day operations and/or specific projects, such as new highways, schools or stadiums.

One of the main benefits of purchasing a municipal bond is that generally speaking the interest is federal tax exempt. In some cases, state and local taxes can also be exempt if you purchase a bond issued in the state you reside in. Due to this beneficial tax treatment the coupon rates are usually less than a taxable issue.

The universe of municipal bonds is split into two different silos. General Obligation (GOs) and Revenue Bonds.

General Obligation (GO)

General obligation bonds are backed by the full faith and credit of the issuer. They are not backed by any specific assets and repayment is based on taxing the residents of the issuing entity. Be it a state, county or city.

Revenue Bonds

Revenue bonds are not repaid by the issuer’s ability to tax. Instead, they are repaid by the revenues generated by the specific entity or project. An example would be tolls generated by a highway project.

When dealing with a revenue bond you need to be aware of the term non-recourse. If a revenue bond is non-recourse and the income stream fades away, the bond holders have no claim to the asset tied to the bond. An example would be if highway tolls drop below a level to pay the bond holders. The bond holders will not have a claim to own the highway and are at risk of losing all of the money invested.

To reduce the risk of total loss, revenue bond buyers can purchase insurance on these bonds. However, this monthly premium will reduce the overall potential return of the bond.

Conduit

In some cases, a municipal borrower will issue a bond for a private entity like a college or hospital. These private entities are then called a “conduit”. The conduit is to pay the municipal borrower who then makes the interest and principal payments for them. If the conduit fails to make payments, the municipal borrower is generally not required to make the missed payments to the bondholders.

Agencies

Agency bonds are issued by two different types of issuers. Federal government agencies and government sponsored enterprises.

Federal Government Agency

A federal agency is created by the U.S. government to regulate or oversee a specific industry or segment of an industry. FHA (Federal Housing Authority), SBA (Small Business Administration), and GNMA (Government National Mortgage Association) are three examples. A federal government agency is similar to a U.S. Treasury security because it has the full faith and credit of the U.S. government behind it. They provide slightly higher interest rates than a U.S. Treasury because of a potential reduction in liquidity.

Government Sponsored Enterprise (GSE)

A GSE is a private company that operates to serve a public purpose. This means they have implied government support and oversight but not the full faith and credit. i.e. The government is not 100% committed or required to save them if they fail. Fannie Mae (Federal National Mortgage Association), Freddie Mac (Federal Home Loan Mortgage), Federal Home Loan Bank, and Federal Farm Credit Bank are examples.

GSE’s also have a higher interest rate than U.S. Treasuries as they have a higher credit risk than U.S. Treasuries due to not being backed by the full faith and credit of the U.S.A. Both issuers tend to pay a semi-annual coupon payment. These coupon payments can be fixed or floating. In some cases, they may even be issued at a discount to par like a T-bill. There can also be preferential tax treatment depending on the issuer.

Sovereigns

A sovereign bond is a bond issued by a government that is not the United States. They too need to raise capital for expenditures and can do it by raising taxes or issuing bonds. The bond can be issued in domestic or foreign currency. The issuers are rated depending on the perceived credit worthiness of the issuing country. A country with a volatile economy, inflation, or other negatives will be required to pay a higher coupon rate.

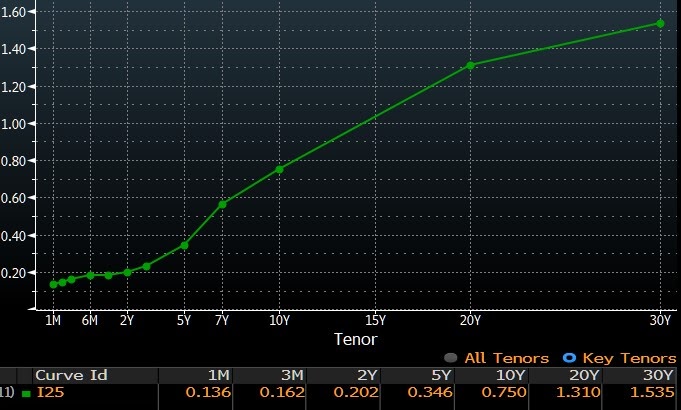

Yield Curve

When you are looking at government bonds one of the best ways to take a quick snapshot view of the landscape is by looking at the yield curve. The yield curve is a graphical representation of each maturity point with the corresponding yield to maturity.

(Source: Bloomberg as of 6/16/20)

In a normal market environment, the yield curve should slope in an upward direction before starting to turn flatter. The shortest maturities will yield the least and as you go farther out in maturity the yields will increase. The current snapshot of the yield curve pictured above represents this state.

The yield curve is a complex subject and we will dedicate a longer blog post to the topic in the future.

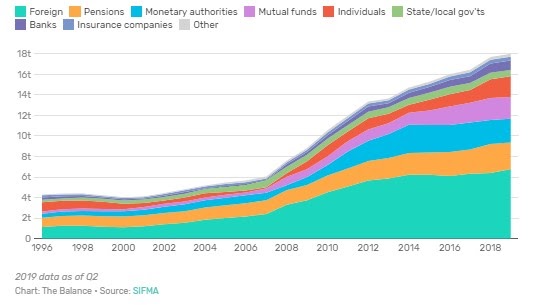

Who Holds US Government Debt and Why?

Government bonds can be held by the issuing governments themselves, their citizens, and other foreign governments. In the United States the holders are classified as intra-governmental debt holders and public holders.

Intra-governmental Holders

Intragovernmental holders in the U.S. are considered to be other federal agencies.

The top of the holder list is the Social Security Fund, aka the U.S. citizen retirement fund. It seems counterintuitive that a government would hold its own debt, but it makes sense. If the Social Security Administration is receiving more funds than they pay out they can’t put that money under their bed. What a large bed that would be! Instead they look to place it in the most secure place possible. In this case it is U.S. Treasury bonds, because U.S. Treasury bonds are backed by the full faith and credit of the U.S. government whose taxing ability keeps the excess cash essentially riskless. As the Social Security Administration needs funds, they can sell the bonds and get the cash back. This type of arrangement is also followed by other government agencies like Medicare & the FDIC.

Public Holders

Foreign governments hold the bulk of the bonds in the public holders’ bucket. Japan and China are the top two, holding $1.27T and $1.08T respectively (source: treasury.gov). Others on the list are the Federal Reserve, mutual funds, government pensions, private pensions, insurance companies, and more.

Foreign governments like to hold large amounts of U.S. government debt for two main reasons. First, by doing so they are able to manage the exchange rate between the U.S. dollar and their own currency. This helps to keep their exports to the United States affordable which helps their economy grow. Second, the U.S Dollar is the reserve currency of the world. This helps the U.S. government remain one of the highest rated issuers in the world.

Risk of Government Bonds

When discussing the risks of government bonds there will be both similarities and differences between U.S. issued debt, other countries, and even corporate issuers. We are dedicating a separate post discussing corporate bonds next in our series.

Because of the United States stellar creditworthiness almost all of the default risk has been removed. What does remain is inflation risk, interest rate risk, and opportunity cost.

Inflation Risk

That same creditworthiness that U.S. government debt provides unfortunately tends to keep the yield on those assets low. Because of this, if inflation starts to increase quickly it can outpace your rate of return. This puts you at a disadvantage if the inflation rate is above the interest rate.

Interest Rate Risk

U.S. government debt actively trades, and prices are impacted by changes in interest rates. If interest rates start to rise, the bond holdings you have will be negatively affected. This is no big deal if you hold your bonds to maturity. On the other hand, if you need to sell, you could see a loss on your principal.

Opportunity Cost

As with any investment there is opportunity cost. If you decide to invest in a government bond for its safety, you likely are giving up an opportunity to invest in a higher returning asset. Add on inflation risk and the opportunity cost you are incurring can be high.

Default Risk

Default risk is almost nonexistent in U.S. government bonds, but other nations are not as fortunate. No nation wants to default on their debt, but it has happened in the past. One of the most recent was Argentina who started missing bond payments in 2001. If you choose strategically you can reduce this risk, but it is out there.

Government Bonds for Corporate Cash Management

The top two rules for corporate cash management are to keep the money as safe as possible and to have it liquid for when it is needed. Government bonds check both boxes. They can be close to riskless thanks to the U.S. government taxing ability and can be liquid in as little as one day in the case of U.S. Treasuries.

We liken them to the strong foundation that is required when constructing a building. Once the base is laid, you can then look elsewhere to increase yield or look for higher income. A corporate cash policy is no different. Lay the foundation and any additions you make in the future will be more sound.

Wrapping Up

This completes the third post in our series entitled, “Bonds – A Primer”. Our next post on corporate bonds will continue to expand on the nuances and intricacies of the bond markets.

Corporate bonds have some similar characteristics to government bonds, but nuanced risk profiles based on the plethora of issuers. This altered risk profile allows corporate cash managers to layer on top of the government bond foundation to reach their yield targets.

InterPrime is always happy to discuss your current corporate cash management policy, so do not hesitate to reach out.