Bonds – A Primer (part 4) - The Corporate Bond Market

In our last post, “The Government Bond Market” we learnt about how the government funds its operations by issuing debt to the public. In this post we are going to review the Corporate Bond Market, one of the largest and most structurally important markets in our modern financial world. This is where corporations from all over the world go to “Borrow Money” in order to finance their capital needs and operations.

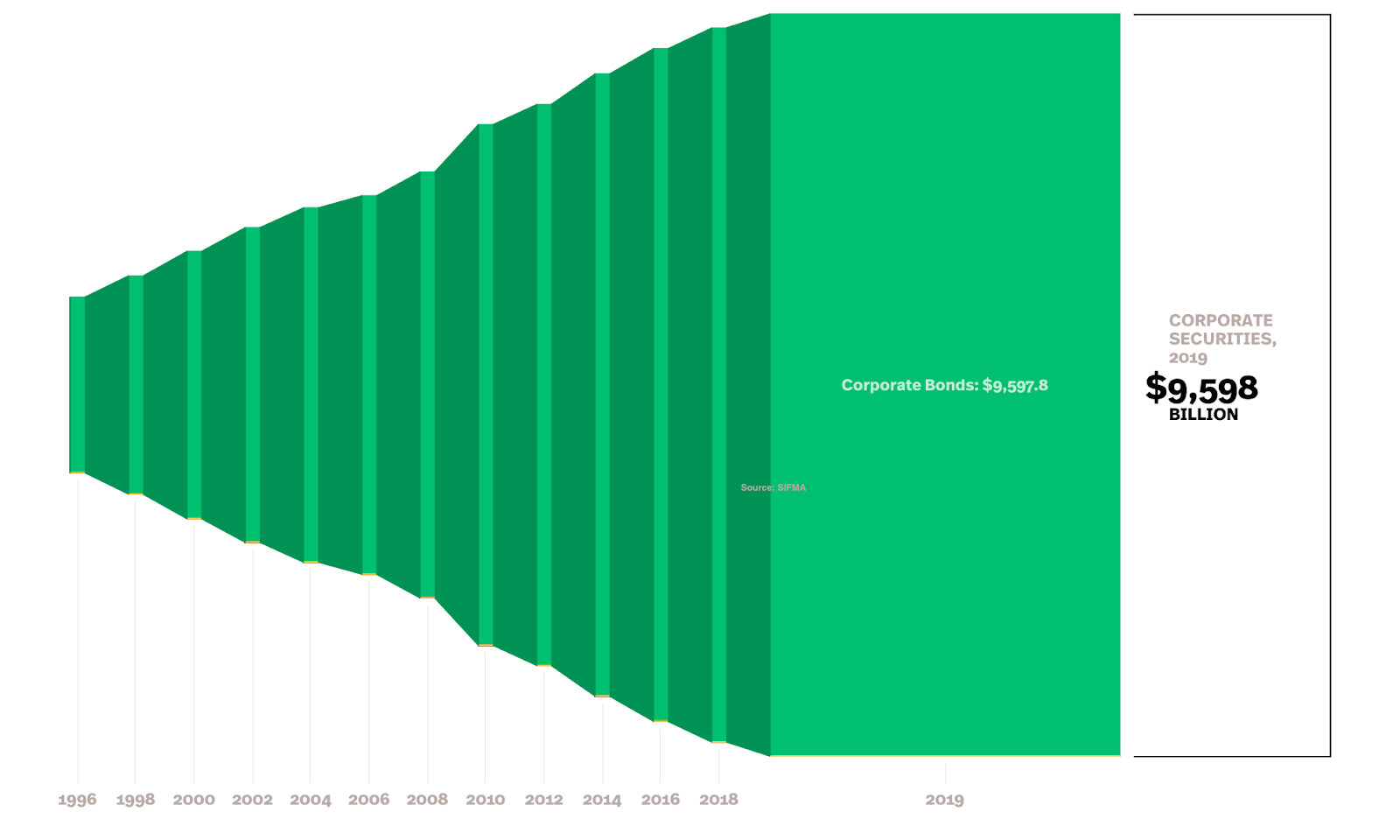

As of May 2020, the Corporate Bond market was over $9.5 Trillion having doubled in size in the last 5 years (Sifma.org).

Source: https://www.sifma.org/resources/research/fixed-income-chart/

Given the importance and size of the market it is critical for corporate cash managers to track & leverage this market.

Understanding the Capital Stack

As a company grows and takes on different forms of debt and financing, a line of who gets paid first is built if things go wrong. This is referred to as the capital stack or capital structure. When investing in corporate bonds it is critical to understand where you stand in “line” to get paid back.

Envision the capital stack like a pyramid or ladder. Those at the top get paid first and it trickles down to the bottom. Those on the bottom can potentially get nothing.

Source: FINRA

When looking at corporate bonds there are several variations of which we need to be aware. This is critical because some bonds are higher on the capital stack than others. We are going to highlight these below.

Senior Secured

The bonds on the top of the capital stack are called senior. The use of the word senior in this instance refers to their position in getting paid. It does not refer to the age of the bond.

When the bond is senior secured that means the issuer has tied collateral to the bond. An example of this would be a large manufacturer using a specific facility, property or equipment to secure the bond debt. In case of default, the senior secured bond holders would have the rights to the collateral and could potentially sell it to recover their funds.

Senior Unsecured and Junior/Subordinated

Next in line on the capital stack to get paid are bonds not secured by collateral. These bonds are referred to as unsecured or debentures. There is no collateral securing the bond. Only the promise of repayment and credit of the issuer.

There is a subclass of bonds in the unsecured bucket called junior or subordinated. These bond holders will only get paid once the senior bond holders receive funds. The term junior is referring to the fact that they are below the more senior position in the capital stack.

Preferred and Common Stock

The final two positions on the capital stack are preferred and common stock.

Preferred stock gives the owner a fixed dividend that will get paid even if a company stops paying the common shareholders. The downside is minimal price appreciation on the shares and the dividend remains fixed without the potential for an increase in dividends.

Common stock is what most investors purchase. You get all of the price appreciation or depreciation of the shares. You may also receive a dividend which is solely at the discretion of the company.

The final difference between the two is that if a company goes bankrupt common stockholders get paid absolutely last in the capital stack. This means common stockholders have the potential of receiving nothing.

Benefits of Corporate Bonds

Above Market Yield

Now that we are in an ultra-low interest rate environment it is becoming more and more difficult to find respectable yield on assets. Government issued bonds are close to zero and if you are in the European markets you may be facing negative rates.

Because a corporate bond is not tied to a government, you receive higher interest rates due to the additional credit risk of the corporate issuer. Below are a few examples of what investment grade corporate bonds with a remaining two-year maturity are yielding versus a US Treasury two-year bond.

US Treasury 2-year note (5/31/22 maturity) is currently yielding 0.20%

- Wells Fargo 3/08/22 maturity is currently yielding 0.71%

- Fifth Third Bank 3/15/22 maturity is currently yielding 0.76%

- Bank of America 5/17/22 maturity is currently yielding 0.79%

(Source: Bloomberg)

Risks of Corporate Bonds

Interest Rate Risk

One of the most important things to understand about bonds is how their prices react to changes in interest rates. Bond prices move opposite to the direction of interest rates. When interest rates are going lower, bond prices are rising. When interest rates are going higher, bond prices are moving lower.

Because of the way bond prices react to interest rates we tend to focus on holding them to maturity. This takes the importance away from the price movements and puts it back on the predictable income payments. For more depth on interest rate risk you can see our previous blog post (add name and link)

Call & Reinvestment Risk

When mortgage rates move lower homeowners can refinance their mortgage to reduce their payment costs. A bond with a call feature, also known as a callable bond, allows a bond issuer to do the same thing as a homeowner. This is called call risk.

The ability for the issuer to “refinance” their bonds means you can potentially lose out on the predictable cash payments you were looking to receive. But it can also mean that you can not replace the bond you had with a new purchase. The inability to replace what was taken away with the called bond is reinvestment risk.

Duration Risk

When you own individual bonds or a bond mutual fund/ETF you take on duration risk.

Put simply, duration is how sensitive a bond price is to changes in interest rates. The larger the coupon payment and the longer a bond has left until it matures will be reflected in more dramatic price swings. i.e. a bond that matures in one year that has a small coupon payment will have less dramatic price gyrations than a bond that matures in 10 years with a larger coupon payment. Duration will always be represented by a number. The higher the number, the more price volatility you can expect when interest rates change.

Issuer Credit & Default Risk

When you make a loan to someone you have the expectation that they will pay you back in a timely fashion. This is no different than when you purchase a bond.

U.S. Treasury bonds are backed by the full faith and credit of the US government. This means the likelihood of not getting paid is close to zero. Some investors even consider them “riskless”.

When purchasing a bond from an individual issuer you have to determine if that issuer is capable of paying now and in the future. The potential of them missing payments and/or not paying at all is called issuer credit and default risk. There are credit rating agencies that grade individual issuers to represent their creditworthiness. We discuss the credit rating agencies and their functions in a later section.

Inflation Risk

The coupon of your bond is the main driver of the yield you will receive. If the coupon on your bond does not pay higher than inflation you are at risk of losing buying power.

A simple example is if your bond pays you a 3% coupon and inflation is running at 4%. You are falling behind inflation by 1%.

Liquidity Risk

While electronic trading systems have made the corporate bond market more liquid, certain bonds do not trade as actively as others. If you happen to purchase a bond that is not actively traded, you risk getting a sub-optimal sale price if you want/need to sell.

Event Risk

Event risk can be classified as a potential one-time event that impacts how investors and rating agencies view a bond issuer. This can impact the desirability of the issuer’s bonds and subsequently the bond price or rating.

Examples of event risk can include potential merger or acquisitions, C-suite indiscretions, natural disasters or geopolitical events.

Bond Ratings and their providers

Almost all bonds will come with an issuer rating. There are currently 10 rating agencies who the SEC has designated as Nationally Recognized Statistical Rating Organizations (NRSROs).

The purpose of these NSROs is to dive deep into each bond issuer and to rate them on a scale starting at AAA (investment grade) down to D (or no grade). They come to these alphabetical rating levels by analyzing issuer financials to determine the probability of them defaulting on their bond payments. Each rating agency uses its own criteria so seeing the same bond with different ratings is not uncommon. Some rating agencies may not even cover all bonds.

Because of these ratings, corporate bonds can be divided into two different classifications. Investment grade and high yield. Generally speaking, investment grade bonds start with a BBB or higher rating. Anything below that is considered high yield or “junk”.

High yield/junk bonds tend to pay you more than investment grade bonds. The reason for this is because the rating agencies have determined that these companies are at higher risk of defaulting on their loan obligations. Due to this higher risk factor the issuers have to pay a higher coupon(rate) to entice investors to purchase their bonds. The closest comparison is to how a credit score can get an individual a better credit card rate or bank loan rate.

Always think twice and do more research when considering a high yield or junk bond. The higher rate of return may come back to bite you.

3 Ways to Use Corporate Bonds for Corporate Cash Management

Because InterPrime focuses mainly on corporate cash management we are going to show you 3 ways we like to use them.

1. Bond Ladder – Payment Matching

A bond ladder is when you buy multiple different bonds with different maturity dates. The goal of doing this is to reduce your risk by having a consistent maturity average and/or match the bond payments to income requirements.

A simple example would be buying bonds in equal dollar amounts with maturities of 2-year, 4-year and 6-year. As the 2-year bond matures you would then purchase a new bond with a maturity 6 years in the future. The original 4-year bond now has 2-years remaining and the original 6-year now has 4. You would continue this process for as long as required.

Another example is an investor who has a consistent corporate payment obligation. They can make a cash payment from an operations account or they could consider purchasing a bond to make the payment for them. How would this work?

You first start with the corporate payment obligation frequency. You then would search for bonds that have a payment frequency to be as close or equal to that obligation payment. From there you would determine how much you would need to invest at the bond’s current yield profile to offset all or part of the obligation payment.

In both of these examples you are using the consistent and predetermined bond payment function to attain a corporate cash goal.

2. Yield Picking – Yield Spread Over US Treasuries

In a previous section we talked about how a corporate bond will pay you a higher interest rate than a government bond. This is because governments have greater probability of repaying their obligation due to taxing power. Therefore, they do not need to pay as high of a coupon.

The difference between what a government bond is paying versus a corporate bond is called the spread. When comparing a government bond to a corporate the spread between the two rates can vary greatly. This discrepancy can lead to some attractive investment opportunities for a corporate cash manager.

A simple example is if a US Treasury 2-year bond is paying 0.50% and an investment grade corporate bond maturing in 2-years is paying you 1.25%. This means the spread is 0.75% in your favor by purchasing the corporate bond. It will also be referred to as “you pick 0.75 versus the Treasury”.

When these types of situations appear, you must consider who the corporate bond issuer is and the probability they will continue to repay their bond debt. If your analysis gives you confidence the corporate issuer can pay their debt you have an opportunity to potentially snag a superior investment yield.

3. Issuer Special Situations

The investing markets are a marvel with the ability to take all available information and price securities in an efficient manner. However, sometimes this does not happen quickly which leads to a corporate bond investing opportunity.

Let’s say a news story comes out on a corporation and it is viewed negatively. This can impact the price of the corporate bonds. A savvy cash manager will see this and start to do due diligence and analysis on the corporate issuer.

After that analysis has been done, the cash manager may deem the news story to be irrelevant to the company’s financial repayment power. They then make a purchase. The news story is ultimately digested by the market as irrelevant and the bond price rebounds. Thus, the cash manager essentially got the bond on sale!

This is admittedly a very basic example, but you get the point. Even bad news can help corporate cash managers find a diamond in the rough.

Wrapping Up

The toolbox of a corporate cash manager is deep. It ranges from simple operational checking accounts to interest rate swaps and currency hedging. Corporate bonds are somewhere in the middle. Having an understanding of how you can use them is critical to attaining cash management goals.

Using corporate bonds allows a corporate cash manager to potentially gain higher interest rates over bank accounts and US Treasuries. They can help you match payment obligations and they can even give you an opportunity to buy an asset on sale.

Some of you may already be using corporate bonds for your cash management needs, and some of you may be thinking about how to leverage them. At InterPrime, we know their value and would love to educate you or work with you to add them to your investment policy. Get in touch for an unbiased conversation and review of your cash management and investment policy.